Notes to the Financial Statements

For the Year Ended 30 June 2015

Note 1: Statement of accounting policies

Reporting entity

The Department of Corrections (the department) is a government department as defined by Section 2 of the Public Finance Act 1989 (PFA). It is domiciled and operates in New Zealand. The relevant legislation governing the department’s operations include the Public Finance Act 1989, the Corrections Act 2004, Corrections Regulations 2005, the State Sector Act 1988, the Sentencing Act 2002, the Parole Act 2002, the Public Safety (Public Protection Orders) Act 2014, and the Bail Act 2000.

The department is a wholly owned entity of the New Zealand Crown whose primary objective is to administer New Zealand’s corrections system in a way that is designed to improve public safety, reduce re-offending and that contributes to the maintenance of a fair and just society.

Statutory authority

The financial statements for the department have been prepared in accordance with the requirements of the Public Finance Act 1989. For the purposes of financial reporting the department is classified as a Public Benefit Entity (PBE).

Reporting period

The reporting period for these financial statements is the year ended 30 June 2015 with comparative figures for the year ended 30 June 2014.

The financial statements were authorised for issue by the Chief Executive of the Department of Corrections on 28 September 2015.

Basis of preparation

The financial statements have been prepared on a going concern basis, and the accounting policies have been consistently applied throughout the period.

Statement of compliance

These financial statements, including comparatives, have been prepared in accordance with Public Sector PBE Accounting Standards (PBE accounting standards) – Tier 1. These standards are based on International Public Sector Accounting Standards (IPSAS). Previously published financial statements have been prepared in accordance with New Zealand equivalents to International Financial Reporting Standards as appropriate for public benefit entities (NZ IFRS (PBE)).

These financial statements, including comparatives, are the first financial statements presented in accordance with the new PBE accounting standards. There were no material adjustments arising on transition to the new PBE accounting standards as explained in Note 19.

Measurement base

The financial statements have been prepared on a historical cost basis, modified by the revaluation of certain non-current assets.

Presentation currency and rounding

The financial statements are presented in New Zealand dollars, rounded to the nearest thousand ($000). The functional currency is New Zealand dollars.

Changes in accounting policies

Accounting policies have been updated to comply with the new PBE accounting standards. Otherwise, there were no changes to the department’s accounting policies during the period.

Standards, amendments and interpretations issued that are not yet effective and have not been early adopted

In May 2013, the External Reporting Board issued a new suite of PBE accounting standards for application by public sector entities for reporting periods beginning on or after 1 July 2014. The department has applied these standards in preparing the 30 June 2015 financial statements.

In October 2014, the PBE suite of accounting standards was updated to incorporate requirements and guidance for the not-for-profit sector. These updated standards apply to PBEs with reporting periods beginning on or after 1 April 2015. The department will apply these updated standards in preparing its 30 June 2016 financial statements. The department expects there will be minimal or no change in applying these updated accounting standards.

Critical judgements and estimates

The preparation of financial statements in conformity with PBE accounting standards requires judgements, estimates and assumptions that affect the application of policies and reported amounts of assets and liabilities, revenue and expenses. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are discussed below.

Retiring and long service leave

An independent actuarial valuation was undertaken by Aon Hewitt as at 30 June 2015 and 2014 to estimate the present value of long service and retiring leave liabilities. The calculations are based on:

- likely future entitlements accruing to staff, based on years of service, years to entitlement, the likelihood that staff will reach the point of entitlement and contractual entitlements information

- the present value of the estimated future cash flows.

Note 14 provides an analysis of the exposure and assumptions in relation to estimates and uncertainties surrounding these liabilities.

Revaluation of land and buildings

Critical judgements in determining the remaining life of land and buildings have been made by the department. Assessing the appropriateness of useful lives and residual values of land and buildings requires consideration of a number of factors such as the physical condition, expected period of use by the department, and expected proceeds from any disposal.

Any property revaluations are certified by an appropriately qualified valuer.

Budget and forecast figures

The budget figures are for the year ended 30 June 2015 and were published in the 2013/14 annual report. They were included in the Estimates of Appropriations for the Government of New Zealand for the year ending 30 June 2015, which are consistent with the financial information in the main estimates. In addition, the financial statements also present the updated budget information from the supplementary estimates.

The forecast figures are for the year ending 30 June 2016, and are consistent with the best estimate financial forecast information submitted to Treasury for the Budget Economic and Fiscal Update (BEFU) 2015 for the 2015/16 year.

The forecast financial statements have been prepared as required by the Public Finance Act (PFA) to communicate forecast financial information for accountability purposes.

The budget and forecast figures have been prepared using the accounting policies adopted in preparing these financial statements.

The forecast figures have been prepared in accordance with PBE FRS 42 Prospective Financial Statements.

The forecast financial statements were authorised for issue by the Chief Executive of the Department of Corrections on 10 April 2015. The Chief Executive is responsible for the forecast financial statements, including the appropriateness of the assumptions underlying them and all other required disclosures.

While the department regularly updates its forecasts, updated forecast financial statements for the year ending 30 June 2016 will not be published.

Significant assumptions used in preparing the forecast financials

The forecast figures contained in these financial statements reflect the department’s purpose and activities and are based on a number of assumptions on what may occur during the 2015/16 year. The forecast figures have been compiled on the basis of existing government policies and ministerial expectations at the time the budget was finalised.

The main assumptions adopted as at 10 April 2015 were as follows:

- the department’s activities and output expectations will remain substantially the same as the previous year focusing on the Government’s priorities

- personnel costs reflect FTE levels consistent with 2014/15

- operating costs are based on historical experience and other factors that are believed to be reasonable in the circumstances and are the department’s best estimate of future costs that will be incurred. Remuneration rates are based on current wages and salary costs, adjusted for anticipated remuneration changes

- land and buildings are not revalued

- muster/demand levels are consistent with 2014/15

- estimated year-end information for 2014/15 was used as the opening position for the 2015/16 forecast.

Significant Accounting Policies

Revenue

Revenue – exchange transactions

Revenue – department and third party

Revenue earned in exchange for the provision of outputs (products or services) to third parties, is recorded as operating revenue.

Revenue from the supply of services is measured at the fair value of consideration received, recognised on a straight-line basis over the specified period for the services unless an alternative method better represents the stage of completion of the transaction.

Revenue from the sale of goods is recognised when the significant risks and rewards of ownership have been transferred to the buyer (usually on delivery of the goods), when the amount of revenue can be measured reliably and it is probable that the economic benefit or service potential associated with the transaction will flow to the entity.

Interest Revenue

Interest revenue is recognised using the effective interest rate method.

Dividend Revenue

Dividend revenue relates to investments arising from the department’s business dealings with companies in the farming industry. Dividend revenue is recognised when the right to receive payment has been established.

Rental Revenue

Rental revenue arising from residential property leases is accounted for on a straight-line basis over the lease terms and included in revenue.

Revenue – non-exchange transactions

Revenue – Crown

Revenue from the Crown is measured based on the department’s funding entitlement for the reporting period. The funding entitlement is established by Parliament when it passes the Appropriation Acts for the financial year. The amount of revenue recognised takes into account any amendments to appropriations approved in the Appropriation (Supplementary Estimates) Act for the year and certain other unconditional funding adjustments formally approved prior to balance date.

There are no conditions attached to the funding from the Crown. However, the department can incur expenses only within the scope and limits of its appropriations.

The fair value of Revenue Crown has been determined to be equivalent to the funding entitlement.

Donated or subsidised assets

Where a physical asset is acquired for nil or nominal consideration, the fair value of the asset received is recognised as revenue when control of the asset is transferred to the department.

Insurance proceeds

Insurance proceeds are recognised when a settlement agreement has been reached which establishes the right to receive payment.

Capital charge

The capital charge is recognised as an expense in the period to which the charge relates.

Finance costs

Finance costs are incurred in relation to the repayment of the service concession arrangement asset design and construction costs over the contract term. Finance costs are recognised as an expense in the period in which they are incurred, except to the extent that they are capitalised under the allowed alternative treatment method. Finance costs that are directly attributable to the construction of a service concession arrangement asset are capitalised as part of the cost of the asset during the construction period.

Cash and cash equivalents

Cash includes cash on hand and cash held in bank accounts and deposits with a maturity of no more than three months.

Debtors and other receivables

Debtors and other receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Receivables are initially recognised at fair value. Receivables with duration of less than 12 months are recognised at their nominal value.

Allowances for estimated irrecoverable amounts are recognised when there is objective evidence that the asset is impaired.

Inventories

Inventories held for resale are measured at the lower of cost (calculated using the weighted average method) and net realisable value. Inventories consumed in providing a service are measured at cost or replacement cost.

Inventories acquired through non-exchange transactions are measured at fair value at the date of acquisition. The amount of any write-down for the loss of service potential or from cost to net realisable value is recognised in surplus or deficit in the period of the write-down.

Property, plant and equipment

Items of property, plant and equipment are shown at cost or valuation, less accumulated depreciation and impairment losses.

Land and buildings

Land and buildings are stated at fair value as determined by an independent registered valuer. Fair value is determined using market-based evidence, except for prison buildings, which are valued at optimised depreciated replacement cost. Land and buildings are revalued at least every three years or whenever the carrying amount differs materially to fair value. Additions between revaluations are initially recorded at cost.

Unrealised gains and losses arising from changes in the value of property, plant and equipment are recognised as at balance date. To the extent that a gain reverses a loss previously charged to surplus or deficit for the asset class, the gain is credited to surplus or deficit. Otherwise, gains are credited to an asset revaluation reserve for that class of asset. To the extent that there is a balance in the asset revaluation reserve for the asset class any loss is debited to the reserve. Otherwise, losses are reported in the Statement of Comprehensive Revenue and Expense.

Accumulated depreciation at revaluation date is eliminated against the gross carrying amount so that the carrying amount after revaluation equals the revalued amount.

Other property, plant and equipment

Other property, plant and equipment, which include motor vehicles and furniture and fittings, are recorded at cost less accumulated depreciation and accumulated impairment losses.

Disposals

Realised gains and losses arising from disposal of property, plant and equipment are recognised in the Statement of Comprehensive Revenue and Expense in the period in which the transaction occurs. When revalued assets are sold or derecognised, the amounts included in asset revaluation reserves in respect of those assets are transferred to general funds.

Service concession arrangements

Service concession arrangements are recognised as assets under construction within property, plant and equipment until the in-service date at which time they are recognised as a separate asset class. As such, service concession arrangements are accounted for in accordance with the department’s policies, which comply with Property, Plant and Equipment PBE IPSAS 17.

For newly constructed assets, the department recognises the asset and corresponding liability, as the asset is being progressively constructed. Service concession arrangements, while under construction, are measured at amortised cost.

Payments made by the department under a service concession arrangement reduce the value of the liability, pay for interest on the principal, reimburse the operator for the service provided and reimburse any other additional operational costs.

Depreciation

Depreciation is charged on a straight-line basis at rates calculated to allocate the cost or valuation of an item of property, plant and equipment, less any residual value, over its estimated useful life. Motor vehicles that have been classified as non-heavy duty have a residual value of 20%.

Typically, the depreciation rates for classes of property, plant and equipment are as follows:

Class of asset | Useful life | Residual value |

Land | Not depreciated | Not applicable |

Buildings | 3 – 75 years | Nil |

Plant and equipment | 5 – 10 years | Nil |

Furniture and fittings | 3 – 5 years | Nil |

Computer hardware | 3 – 10 years | Nil |

Motor vehicles | 5 – 8 years | 20% |

Service concession arrangements | ||

Land | Not depreciated | Not applicable |

Buildings | 7 – 65 years | Nil |

Plant and equipment | 3 – 10 years | Nil |

The useful life of buildings is reassessed following any revaluation.

Leasehold improvements are depreciated over the unexpired period of the lease or the estimated remaining useful life of the leasehold improvement, whichever is the shorter.

Intangible assets

Software acquisition and development

Acquired computer software licenses are capitalised, where appropriate, on the basis of the costs incurred to acquire and bring to use the specific software.

Costs associated with maintaining computer software and training staff are recognised as an expense when incurred.

Direct costs that are associated with the development of software for internal use by the department, are recognised as an intangible asset. Direct costs include the software development, employee costs and an appropriate portion of the relevant indirect and overhead costs.

Amortisation

The carrying value of an intangible asset with a finite life is amortised on a straight-line basis over its useful life. Amortisation begins when the asset is available for use and ceases at the date that the asset is derecognised. The amortisation charge for each period is recognised in the Statement of Comprehensive Revenue and Expense.

The useful lives and associated amortisation rates of major classes of intangible assets have been estimated as follows:

Class of asset | Useful life | Residual value |

Acquired/internally generated software | 3 – 10 years | Nil |

Biological assets

Biological assets are initially recorded at fair value less costs associated with the sale or disposal of those assets.

Forestry

Forestry assets are independently revalued on an annual basis. Fair value is determined based on the present value of expected net cash flows discounted at a current market determined post-tax rate.

Gains or losses arising from a change in fair value less costs associated with the sale or disposal of those assets are recognised in the Statement of Comprehensive Revenue and Expense.

The costs to maintain forestry assets are included in the Statement of Comprehensive Revenue and Expense.

Livestock

Livestock assets are recorded at fair value less costs associated with the sale or disposal of those assets. Gains or losses due to changes in the per head value of livestock and changes in livestock numbers, are recognised in the Statement of Comprehensive Revenue and Expense.

Investments

Investments are initially recognised at cost being the fair value of consideration given. All investments are subsequently carried at fair value. Any changes in fair value are recognised in the Statement of Comprehensive Revenue and Expense in the period in which they arise.

Fair value for investments is determined as follows:

- listed shares are valued at the quoted price at the close of business on the balance date

- non-listed shares are recognised at initial cost of investment and adjusted for performance of the business since that date.

Impairment of non-financial assets

Cash-generating assets

The department does not hold any cash-generating assets. Assets are considered cash-generating where their primary objective is to generate a commercial return. The department holds some commercial assets with the primary objective of providing employment and training opportunities to prisoners as part of rehabilitation and reintegration programmes.

Non-cash-generating assets

Assets that have an indefinite useful life are not subject to amortisation and are tested annually for impairment. An intangible asset that is not yet available for use at balance date is tested for impairment annually.

Assets held at cost that have a finite useful life are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised when the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell or its value in use.

Value in use is the depreciated replacement cost for an asset where the future economic benefits or service potential of the asset is not primarily dependent on the asset’s ability to generate net cash inflows and where the department would, if deprived of the asset, replace its remaining future economic benefits or service potential.

If an asset’s carrying amount exceeds its recoverable service amount, the asset is regarded as impaired and the carrying amount is written down to the recoverable amount. The total impairment loss is recognised in the surplus or deficit.

The reversal of an impairment loss is recognised in the surplus or deficit.

Employee entitlements

Employee entitlements to salaries and wages, annual leave, long service leave and other similar benefits are recognised in the Statement of Comprehensive Revenue and Expense when they accrue to employees. Employee entitlements that the department expects to be settled within 12 months of balance date are measured at nominal values based on accrued entitlements at current rates of pay. The liability for long-term employee entitlements is reported as the present value of estimated future cash outflows.

Termination benefits

Termination benefits are recognised in the Statement of Comprehensive Revenue and Expense only when there is a demonstrable commitment to either terminate employment prior to normal retirement date or to provide such benefits as a result of an offer to encourage voluntary redundancy. Termination benefits settled within 12 months are reported at the amount expected to be paid. Termination benefits not expected to be settled within 12 months are reported as the present value of the estimated future cash outflows.

Defined contribution schemes

Obligations for contributions to KiwiSaver, the Government Superannuation Fund, and other defined contribution superannuation schemes are recognised as an expense in the Statement of Comprehensive Revenue and Expense as they are incurred.

Foreign currency

Transactions in foreign currencies are translated at the foreign exchange rate at the date of the transaction. Foreign exchange gains or losses resulting from the settlement of these transactions are recognised in the Statement of Comprehensive Revenue and Expense.

Monetary assets and liabilities denominated in foreign currencies at balance date are translated to New Zealand dollars at the foreign exchange rate at balance date. Foreign exchange gains or losses arising from translation of monetary assets and liabilities are recognised in the Statement of Comprehensive Revenue and Expense.

Financial instruments

The department is party to financial instruments as part of its normal operations. These financial instruments consist of cash and cash equivalents, debtors and other receivables, investments, creditors and other payables and other financial liabilities.

All financial instruments are initially measured at fair value plus transaction costs, unless they are carried at fair value through the Statement of Comprehensive Revenue and Expense, in which case the transaction costs are recognised in surplus or deficit. Financial assets designated at fair value through surplus or deficit are recorded at fair value with any realised and unrealised gains or losses recognised in the Statement of Comprehensive Revenue and Expense.

Other financial liabilities greater than 12 months are subsequently measured at amortised cost using the effective interest rate method. Financial liabilities entered into with duration less than 12 months are recognised at their nominal value.

Provisions

The department recognises a provision for future expenditure of an uncertain amount or timing when:

- there is a present obligation (either legal or constructive) as a result of a past event

- it is probable that an outflow of future economic benefits will be required to settle the obligation, and

- a reliable estimate can be made of the amount of the obligation.

Provisions are not recognised for net deficits from future operating activities. Provisions are measured at the present value of the expenditure expected to be required to settle the obligation using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the obligation. Any increases in the provision due to the passage of time would be recognised as a finance cost.

Accident Compensation Corporation (ACC) Partnership Programme

The department belongs to the ACC Partnership Programme whereby the department accepts the management and financial responsibility of work-related illnesses and accidents of employees.

Under the programme, the department is liable for the costs of all claims for a period of five years. At the end of the five year period, the department pays a premium to ACC for the value of residual claims, and the liability for ongoing claims passes to ACC from that point.

The liability for the programme is measured at the present value of expected future payments to be made in respect of the employee injuries and claims up to the reporting date using actuarial techniques. Consideration is given to expected future wage and salary levels and experience of employee claims and injuries. Expected future payments are discounted using market yields at the reporting date on government bonds with terms to maturity that match, as closely as possible, the estimated future cash outflows.

Onerous contracts

Where the benefits to be derived from a contract are lower than the unavoidable costs of meeting the obligation under the contract, a provision is recognised. The provision is stated at the present value of the future net cash outflows expected to be incurred in respect of the contract.

Taxation

Income tax

Government departments are exempt from income tax as public authorities. Accordingly, no charge for income tax has been provided for.

Goods and services tax (GST)

All statements are GST exclusive, except for creditors and other payables and debtors and other receivables within the Statement of Financial Position. These amounts are shown as GST inclusive.

The net amount of GST payable to, or recoverable from Inland Revenue (IR) at balance date is included in creditors or debtors as appropriate. The net amount of GST paid to, or received from IR including GST relating to investing and financing activities is classified as an operating cash flow in the Statement of Cash Flows.

Operating leases

Leases, where the lessor substantially retains the risks and rewards of ownership, are recognised in a systematic manner over the term of the lease.

Leasehold improvements are capitalised and the cost is amortised over the unexpired period of the lease or the estimated useful life of the improvements, whichever is shorter.

Commitments

Future expenses and liabilities to be incurred on capital contracts and non-cancellable operating leases that have been entered into at balance date are disclosed as commitments to the extent they represent unperformed obligations.

Contingent liabilities

Contingent liabilities are disclosed in the Statement of Contingent Liabilities at the point at which the contingency is evident. Contingent liabilities are not disclosed if the possibility of an outflow of resources embodying economic resources is remote.

Contingent assets

Contingent assets are disclosed in the Statement of Contingent Assets at the point at which an inflow of economic benefits or service potential is probable.

Cost accounting policies

The department has determined the costs of outputs using the cost allocation system outlined below.

Cost allocation

Costs that are driven by prisoner or offender related activities are recognised as direct costs and assigned to outputs. Direct costs are charged to outputs based on actual consumption or activity analysis. Pre-established ratios have been used in some instances, which are reviewed at regular intervals.

Indirect costs are driven by organisational support functions and are not directly related to prisoner or offender activities. Indirect costs are allocated to outputs based on appropriate resource consumption and/or activity analysis.

Changes in cost accounting policies

There have been no changes in cost accounting policies during the period.

Note 2: Other revenue

2014 Actual $000 | 2015 Actual $000 | |

37,201 | Sale of goods | 35,388 |

3,552 | Board and rents | 3,410 |

143 | Profit on sale of assets | 3,454 |

– | Insurance proceeds | 4,508 |

474 | Revenue other | 17 |

41,370 | Total other revenue | 46,777 |

Sale of goods mainly comprises revenue from offender employment activities such as farming and forestry.

Insurance proceeds relate to settlement of claims for the 2012 Christchurch earthquake ($3.3 million) and the 2013 Spring Hill Corrections Facility riot ($1.2 million).

Note 3: Personnel costs

2014 Actual $000 | 2015 Actual $000 | 2015 Budget (unaudited) $000 | 2016 Forecast* (unaudited) $000 | |

522,218 | Salaries and wages | 521,051 | 526,539 | 524,402 |

1,237 | ACC Partnership Programme | 936 | – | – |

408 | Government Superannuation Fund contribution expense | 350 | 280 | 243 |

13,271 | State Sector Retirement Savings Scheme and KiwiSaver employer contribution | 13,583 | 14,449 | 13,630 |

1,230 | Retiring and long service leave | 1,641 | 1,797 | 1,641 |

1,120 | Termination benefits | 6,497 | – | – |

539,484 | Total personnel costs | 544,058 | 543,065 | 539,916 |

* Forecast financial statements have been prepared using Budget Economic Fiscal Update (BEFU) 2015

Note 4: Operating costs

2014 Actual $000 | 2015 Actual $000 | 2015 Budget (unaudited) $000 | 2016 Forecast* (unaudited) $000 | |

17,205 | Operating lease rentals | 16,739 | 16,827 | 17,500 |

366 | Audit fees for annual audit | 370 | 361 | 370 |

50 | Fees to auditors for other services | 39 | – | – |

76,723 | Facilities maintenance | 71,825 | 76,475 | 70,125 |

57,551 | Offender management costs | 55,506 | 58,161 | 53,693 |

34,378 | Information technology costs | 32,246 | 33,589 | 33,165 |

66,661 | Contract management | 86,680 | 77,018 | 107,670 |

29,458 | Administration | 24,383 | 23,148 | 25,236 |

168 | Receivables written off during period | 7 | – | – |

10,069 | Inventory expenses | 9,104 | 9,033 | 9,022 |

46,577 | Other operating costs | 47,492 | 18,330 | 29,342 |

3,328 | Loss on sale of assets | 2,396 | – | – |

| 342,534 | Total operating costs | 346,787 | 312,942 | 346,123 |

* Forecast financial statements have been prepared using Budget Economic Fiscal Update (BEFU) 2015

Note 5: Capital charge

The department pays a capital charge to the Crown on its taxpayers’ funds as at 30 June and 31 December each year. The capital charge rate for the year ended 30 June 2015 was 8% per annum (2014: 8% per annum).

Note 6: Cash and cash equivalents

| 2014 Actual $000 | 2015 Actual $000 | |

| 82,337 | Cash and bank balances | 58,459 |

| 82,337 | Total cash and cash equivalents | 58,459 |

The department is required by the Treasury to maintain a positive balance in its bank accounts at all times. The department has two bank accounts with Westpac New Zealand Limited.

Note 7: Debtors and other receivables

2014 Actual $000 | 2015 Actual $000 | |

Current portion | ||

Exchange transactions | ||

4,453 | Trade debtors – external | 1,554 |

189 | Employee advances | 207 |

(24) | Less provision for impairment | (6) |

4,618 | Trade debtors – external and employees | 1,755 |

2,253 | Trade debtors – other government entities | 1,312 |

2,253 | Trade debtors – other government entities | 1,312 |

Non-exchange transactions | ||

381,469 | Debtor Crown | 337,839 |

381,469 | Debtor Crown | 337,839 |

– | Trade debtors – external | 3,296 |

– | Trade debtors – external | 3,296 |

388,340 | Total debtors and other receivables | 344,202 |

The carrying value of trade debtors approximates their fair value.

The debtor Crown of $337.8 million (2014: $381.5 million) consists of operating funding (GST inclusive) not drawn down as a result of the timing of cash requirements.

There is minimal credit risk with respect to external receivables. The department’s standard terms of credit are that payment is due on the 20th of the month following the date of invoice. No further extension of credit is permitted.

All debtors are expected to be realised within 12 months and therefore classified as current. The department classifies debtor Crown as current because it can be realised in cash within three working days.

Trade debtors relating to non-exchange transactions represents the balance of insurance proceeds owed in relation to the 2012 Christchurch earthquake.

The ageing profile of debtors and other receivables at year-end is detailed below:

Gross $000 | 2014 Impairment $000 | Net $000 | Gross $000 | 2015 Impairment $000 | Net $000 | |

Not past due | 386,847 | – | 386,847 | 342,255 | – | 342,255 |

Past due 1-30 days | 1,283 | – | 1,283 | 1,164 | – | 1,164 |

Past due 31-60 days | 65 | – | 65 | 441 | – | 441 |

Past due 61-90 days | 41 | (24) | 17 | 151 | – | 151 |

Past due > 90 days | 128 | – | 128 | 197 | (6) | 191 |

388,364 | (24) | 388,340 | 344,208 | (6) | 344,202 |

As at 30 June 2015 (and 30 June 2014), all overdue receivables were assessed for impairment and appropriate provisions applied. Movements in the provision for impairment of debtors and other receivables are as follows:

2014 Actual $000 | 2015 Actual $000 | |

71 | Balance at 1 July | 24 |

(47) | Provisions released during the year | (18) |

24 | Balance at 30 June | 6 |

The provision for impairment of debtors has been calculated based on expected losses for the department’s pool of debtors. Expected losses have been determined based on analysis of the department’s losses in previous periods, and review of specific debtors.

Those specific debtors that are insolvent are fully provided for. As at 30 June 2015 the department had no debtors that were insolvent (2014: Nil).

Note 8: Inventories

2014 Actual $000 | 2015 Actual $000 | |

3,448 | Inventory held for the provision of goods and services | 3,328 |

657 | Finished goods | 549 |

4,105 | Total inventories | 3,877 |

The department’s inventory consists of supplies that are available for prisoner purchases, operational supplies and inventory held for use in prisoner employment. No inventories are pledged as security for liabilities.

All inventories are expected to be realised within 12 months and are therefore classified as current.

Note 9: Investments

2014 Actual $000 | 2015 Actual $000 | |

Non-current portion | ||

7,130 | Investments | 6,064 |

7,130 | Total investments | 6,064 |

Investments arise from the department’s business dealings with companies in the farming industry, mainly shares in Fonterra Co-operative Group Limited. These investments are classified as financial instruments and valued at fair value through the Statement of Comprehensive Revenue and Expense.

The department classifies investments that are expected to be realised within 12 months as current.

Note 10: Property, plant and equipment

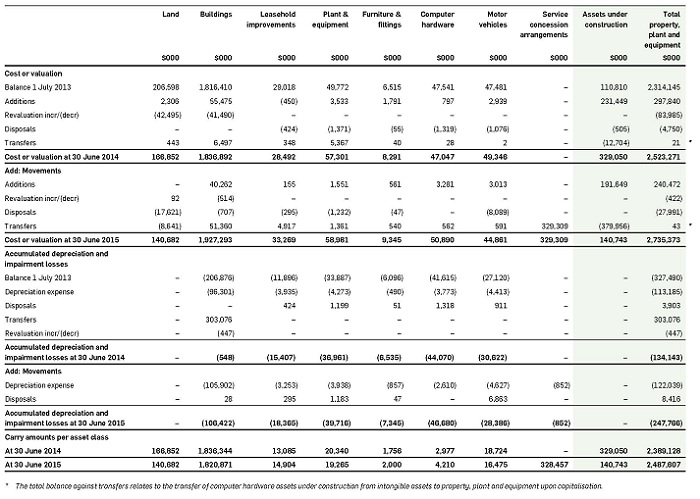

An independent valuer, Beca Group, performed the most recent valuation of freehold land and buildings and the valuation was effective as at 30 June 2014. Nigel Hoskin B.B.S (VPM), ANZIV certified this valuation. The total fair value of freehold land and buildings valued by Beca Group at 30 June 2014 was $1,998 million.

The department has land holdings that are subject to Treaty of Waitangi claims and therefore there may be restrictions on disposal unless under Treaty claim procedures. No adjustment has been made to the value of the department land holdings, to reflect these restrictions.

The department classifies property, plant and equipment expected to be sold in the next 12 months as assets held for sale.

The department constructs prison buildings, which are classified as assets under construction. Assets under construction are capitalised at the in-service date. Assets under construction includes buildings $134.4 million (2014: $91.4 million), leasehold improvements $6.3 million (2014: $6.4 million) and service concession arrangements Nil (2014: $231.3 million).

The department currently holds residential properties that were purchased in the 1960s. The department holds these properties so that it is able to provide accommodation to staff working in prisons located in rural areas. The rental revenue that is received from these properties is incidental, as opposed to being held for investment purposes. The net carrying amount of these properties is $1.5 million (2014: $2.1 million).

The department holds the Old Prison at Mt Eden Corrections Facility as a heritage asset. The department does not recognise heritage assets within property, plant and equipment, however, it is insured under the department’s material damage policy for an estimated total reinstatement value of $102.1 million.

There are no restrictions over the title of the department’s property, plant and equipment, nor are any property, plant and equipment pledged as security for liabilities.

Service concession arrangements

Operations at the new 960 bed Auckland South Corrections Facility commenced in May 2015. The facility was designed, financed and built through a Public Private Partnership with SecureFuture Wiri Limited (contractor). Under the agreement the department provided existing department owned land, adjacent to the Auckland Region Women’s Corrections Facility to the contractor on which to build the prison. SecureFuture will continue to operate and maintain the prison for a period of 25 years, after which responsibility for ongoing maintenance and operation will revert to the department. The Chief Executive of the Department of Corrections will be responsible for the safe, secure and humane containment of prisoners on that site.

The service concession arrangements asset comprises land $8.7 million, buildings $300.5 million and plant and equipment $19.3 million.

During the year finance costs of $18 million were capitalised during the construction period (2014: $10.8 million).

Under this agreement the department pays a monthly unitary charge to the contractor from service commencement. This charge covers, and is allocated between:

- the construction of the prison – these costs are not repriced and are recognised as a reduction against the service concession liability. Repayment of the service concession liability will be over a term of 25 years from service commencement at an effective interest rate of 6.1% per annum. Certain major capital expenditure incurred (such as re-roofing, replacement of heating units) during the term of the agreement is paid for by the department at the time it is provided by the contractor, and the unitary charge is adjusted at this time for these amounts

- the finance costs – finance costs are repriced every five years and the amount the department pays to the contractor is adjusted. Finance charges are recognised as an expense using the effective interest rate

- the service costs – these costs cover operation of the prison as well as routine repairs and maintenance required to keep the prison operational and in good condition. A portion of these costs is indexed to Consumer Price Index and Labour Cost Index. This portion can be reset at year five and year fifteen of the agreement. Any change in these service costs will result in a change to the amount the department pays to the contractor. Service costs are recognised as an expense in the period incurred.

Termination clauses and penalties are outlined in the department’s base agreement and there is no right of renewal after the 25 years.

Note 11: Intangible assets

Acquired software$000 | Internally generated software$000 | Assets under construction$000 | Total intangible assets$000 | |

Cost or valuation | ||||

Balance 1 July 2013 | 24,959 | 56,406 | 33,020 | 114,385 |

Additions | 1,939 | 2,001 | 17,078 | 21,018 |

Disposals | (952) | (748) | (1,934) | (3,634) |

Transfers | 6,990 | 4,366 | (11,377) | (21)* |

Cost or valuation at 30 June 2014 | 32,936 | 62,025 | 36,787 | 131,748 |

Add: Movements | ||||

Additions | 206 | 5,702 | 16,817 | 22,725 |

Disposals | – | – | (2,071) | (2,071) |

Transfers | 3,896 | 22,185 | (26,124) | (43)* |

Cost or valuation at 30 June 2015 | 37,038 | 89,912 | 25,409 | 152,359 |

Accumulated depreciation and impairment losses | ||||

Balance 1 July 2013 | (19,807) | (35,978) | – | (55,785) |

Amortisation expense | (3,167) | (6,049) | – | (9,216) |

Disposals/transfers | 494 | 455 | – | 949 |

Accumulated depreciation and impairment losses at 30 June 2014 | (22,480) | (41,572) | – | (64,052) |

Add: Movements | ||||

Amortisation expense | (3,084) | (9,019) | – | (12,103) |

Accumulated depreciation and impairment losses at 30 June 2015 | (25,564) | (50,591) | – | (76,155) |

Carrying amounts | ||||

At 30 June 2014 | 10,456 | 20,453 | 36,787 | 67,696 |

At 30 June 2015 | 11,474 | 39,321 | 25,409 | 76,204 |

* The total balance against transfers relates to the transfer of computer hardware assets under construction from intangible assets to property, plant and equipment upon capitalisation.

The department develops and maintains internally generated software, which are classified as assets under construction and capitalised at the in-service date. There are no restrictions over the title of the department’s intangible assets, nor are any intangible assets pledged as security for liabilities.

Note 12: Biological assets

Forest crop $000 | Livestock $000 | Total biological assets $000 | |

Cost or valuation | |||

Balance at 1 July 2014 | 40,554 | 12,669 | 53,223 |

Purchases | – | 224 | 224 |

Net gain/(loss) due to: regeneration, maturation and changes in unit values | 751 | 6,779 | 7,530 |

Sales/harvest | (8,465) | (9,579) | (18,044) |

Disposal of forest crop | (32,840) | – | (32,840) |

Cost or valuation at 30 June 2015 | – | 10,093 | 10,093 |

Net change | (40,554) | (2,576) | (43,130) |

Change due to disposal of forest crop | (32,840) | – | (32,840) |

Change due to movement in quantity | – | (1,383) | (1,383) |

Change due to movement in fair value | (7,714) | (1,193) | (8,907) |

Carrying amounts | |||

At 30 June 2014 | 40,554 | 12,669 | 53,223 |

At 30 June 2015 | – | 10,093 | 10,093 |

There are no restrictions over the title of the department’s biological assets, nor are any biological assets pledged as security for liabilities.

Forests

The department sold the Tongariro/Rangipo forest crop and land to the Central North Island Forests Iwi Collective (the collective) under a treaty settlement on 30 June 2015. A robust and independent valuation process was agreed and undertaken by both parties. The Crown Forestry unit within the Ministry for Primary Industries was involved throughout the process including the review of both valuations. This process resulted in an agreed settlement price of the valuation midpoint, which reflected fair value at the date of settlement.

Livestock

The department farms sheep, cattle, deer and pigs at various locations throughout New Zealand. At 30 June 2015, livestock on hand comprised 12,078 sheep (2014: 14,491); 731 beef cattle (2014: 1,692); 4,404 dairy cattle (2014: 4,463); 2,605 deer (2014: 2,740) and 7,492 pigs (2014: 7,191).

The valuation of livestock is based on the active market price and was undertaken by various independent livestock valuers. The overall decrease in the number of livestock was primarily due to the de-stocking at the Tongariro/Rangipo farm in preparation for settlement with the collective.

Financial risk management strategies

The department is exposed to financial risks arising from changes in commodity prices, in particular the price of milk solids. However the financial risk is not considered to be material. The department reviews its outlook for livestock and milk prices regularly in considering the need for active financial risk management.

Note 13: Creditors and other payables

2014 Actual $000 | 2015 Actual $000 | |

Current portion | ||

Exchange transactions | ||

22,778 | Trade creditors | 14,119 |

87,117 | Accrued expenditure | 80,863 |

Non-exchange transactions | ||

9,854 | GST payable | 9,312 |

119,749 | Total creditors and other payables | 104,294 |

Creditors and other payables are non-interest bearing and are normally settled on 30 day terms. Therefore, the carrying value of creditors and payables approximates their fair value.

The department classifies creditors and other payables that are expected to be settled within 12 months as current.

Note 14: Employee entitlements

2014 Actual $000 | 2015 Actual $000 | |

Current liabilities | ||

23,305 | Retiring and long service leave* | 24,572 |

50,485 | Annual leave | 52,066 |

1,632 | Sick leave | 2,327 |

75,422 | Total current portion | 78,965 |

Non-current liabilities | ||

13,580 | Retiring and long service leave* | 16,025 |

13,580 | Total non-current portion | 16,025 |

89,002 | Total provision for employee entitlements | 94,990 |

* Retiring and long service leave liabilities include $2.1 million relating to the impact of a reduction in the discount rates assumed in the actuarial valuation.

Employee entitlements, expected to be settled within 12 months of balance date, are measured at nominal values based on accrued entitlements at current rates of pay. These include annual leave earned, but not taken at balance date, retiring and long service leave entitlements expected to be settled within 12 months and sick leave.

The department classifies employee entitlements as current that:

- are expected to be settled within 12 months after the balance date; and

- the department does not have an unconditional right to defer settlement of the liability for at least 12 months after the balance date.

The present value of the retiring and long service leave obligations depend on multiple factors that are determined on an actuarial basis using a number of assumptions. Two key assumptions used in calculating this liability are the discount rates and the salary inflation factor. Any changes in these assumptions will impact on the carrying amount of the liability.

Independent valuer Marcelo Lardies, a member of the New Zealand Society of Actuaries, from Aon Hewitt, valued retiring and long service leave as at 30 June 2015 (2014: Greg Lee from Aon Hewitt).

The major assumptions used in the 30 June 2015 valuation are that future salary growth rates are 3.00% (2014: 3.00%) per annum and discount rates ranged from 3.18% to 5.50% (2014: 3.42% to 5.50%) per annum.

In determining the appropriate discount rates, the valuer used the weighted averages of returns on government stock of different terms to maturity that match, as closely as possible, the estimated future cash outflows. The salary growth assumption is consistent with the results of the Aon Economists’ Survey.

Note 15: Provisions

2014 Total provisions Actual $000 | 2015 Restructuring Actual $000 | 2015 Employee accidents Actual $000 | 2015 Other provisions Actual $000 | 2015 Total provisions Actual $000 | |

Current provisions | |||||

6,655 | Balance at 1 July | 773 | 5,483 | 577 | 6,833 |

2,518 | Additional provisions made during the year | 5,557 | 989 | 394 | 6,940 |

(1,475) | Charged against provision for the year | (709) | (530) | (180) | (1,419) |

(865) | Provision reversed during the year | (64) | – | (59) | (123) |

6,833 | Current provisions | 5,557 | 5,942 | 732 | 12,231 |

6,833 | Total provisions | 5,557 | 5,942 | 732 | 12,231 |

Restructuring

The 2015 provision relates to the Lifting Productivity and Performance in New Zealand’s Prisons restructure announced in May 2015. The restructure is centred on unifying the prison resources and closing individual facilities at Waikeria, Tongariro/Rangipo and Rimutaka prisons which are no longer fit for purpose. The prison unit closures will commence in 2015/16 and are scheduled to be fully completed by April 2016.

The 2014 restructuring provision related to the Lifting our Productivity Programme and the 2012 organisation realignment which resulted in disestablished positions. The restructuring was completed during the current year.

Employee accidents

The provision relates to the estimation of the department’s outstanding claims liability under the ACC Partnership Programme. An external independent actuarial valuer, Mark Weaver (Fellow of the New Zealand Society of Actuaries) from Melville Jessup Weaver provided an estimate of the outstanding claims liability as at 30 June 2015 and 2014.

Key assumptions

The key assumptions used in determining the value of outstanding claims are:

- the development pattern of claims payments is the same for all loss periods. That is, the future claims pattern will reflect that which occurred in the past

- the assumed loss ratios were determined by considering the observed loss ratios for developed loss quarters

- the discount rates were based on government bond yields published by the Reserve Bank of New Zealand

- the department will remain in the ACC Accredited NZ Employers Programme (ACCEP) for the foreseeable future. If the department were to exit immediately, a risk margin of 12.8% (2014: 12.0%) per annum would be added by ACC.

The estimated ACCEP outstanding claims liability as at 30 June 2015 included a provision for future claims handling expenses of 10.8% (2014: 11.2%) per annum of expected future claims costs.

Other provisions

Parental leave

The department provides an ex-gratia payment to employees (approximating six weeks pay) who return to Corrections for a period of time (as specified in contracts typically three to six months) after being on parental leave. The department anticipates that this provision will be realised within 12 months.

Onerous leases

The provision for onerous contracts arises from a non-cancellable lease where the unavoidable costs of meeting the lease contract exceed the economic benefits to be received from it. The department has a number of operating lease contracts. This provision represents the future estimated irrecoverable expenses for vacant leased premises. The department has between one to three years remaining on these leases.

Note 16: Provision for repayment of surplus to the Crown

2014 Actual $000 | 2015 Actual $000 | |

30,326 | Net surplus | 1,974 |

Plus/(minus) | ||

(4,480) | Unrealised decrease/(increase) in fair value of biological assets | 1,193 |

1,719 | Unrealised decrease/(increase) in fair value of shares | 1,084 |

– | Unrealised change in discount rates for retiring and long service leave | 2,071 |

27,565 | Provision for repayment of surplus to the Crown | 6,322 |

Remeasurements that are reported in the Statement of Comprehensive Revenue and Expense mainly relate to unrealised changes in fair value as a result of revaluation. Under the Public Finance Act 1989 all remeasurements are exempted from the requirement for appropriation on the basis of a lack of control. Similarly, unrealised remeasurements are not intended to affect the surplus repayable to the Crown.

The return of surplus to the Crown is required to be paid by 31 October of each year.

Note 17: Taxpayers’ funds

Taxpayers’ funds comprise general funds, revaluation reserves and fair value through other comprehensive revenue and expense reserves.

2014 Actual $000 | 2015 Actual $000 | |

General funds | ||

1,753,732 | Balance at 1 July | 1,759,693 |

30,326 | Net surplus | 1,974 |

– | Transfer from fair value through equity reserve | 2,267 |

3,200 | Capital contribution from the Crown | – |

– | Capital returned to the Crown | (63,967) |

33,526 | Total movement in general funds | (59,726) |

(27,565) | Provision for repayment of surplus to the Crown (Note 16) | (6,322) |

1,759,693 | Balance at 30 June | 1,693,645 |

Revaluation reserves | ||

538,846 | Balance at 1 July | 757,490 |

218,644 | Revaluation (losses)/gains | (422) |

757,490 | Balance at 30 June | 757,068 |

Fair value through equity reserve | ||

2,267 | Balance at 1 July | 2,267 |

– | Transfer to general funds | (2,267) |

2,267 | Balance at 30 June | – |

759,757 | Reserves total | 757,068 |

2,519,450 | Total taxpayers’ funds at 30 June | 2,450,713 |

The department has no restricted reserves.

The transfer from fair value through equity reserve to general funds relates to an asset disposed of in a prior period.

Capital returned to the Crown mainly relates to the Tongariro/Rangipo forest crop and land sale proceeds and the departments’ contribution to the Justice Sector precinct land purchase in Christchurch.

2014 Actual $000 | 2015 Actual $000 | |

Revaluation reserves | ||

Land | ||

135,271 | Revaluation reserves at 1 July | 92,776 |

(42,495) | Revaluation gains/(losses) | 92 |

92,776 | Revaluation reserves at 30 June | 92,868 |

Buildings | ||

403,575 | Revaluation reserves at 1 July | 664,714 |

261,139 | Revaluation (losses)/gains | (514) |

664,714 | Revaluation reserves at 30 June | 664,200 |

757,490 | Total reserves at 30 June | 757,068 |

Fair value through equity reserve | ||

2,267 | Revaluation reserves at 1 July | 2,267 |

– | Transfer to general funds | (2,267) |

2,267 | Revaluation reserves at 30 June | – |

759,757 | Total reserves at 30 June | 757,068 |

Note 18: Reconciliation of net surplus to net cash flow from operating activities

2014 Actual $000 | 2015 Actual $000 | |

30,326 | Net surplus | 1,974 |

Add/(less) non-cash items | ||

122,401 | Depreciation and amortisation | 134,142 |

– | Dividends received | (18) |

(74) | Non-current employee entitlements | 2,445 |

122,327 | Total non-cash items | 136,569 |

(Increase)/decrease in working capital | ||

(60,678) | Debtors and other receivables | 44,138 |

200 | Inventories | 228 |

2,921 | Prepayments | (331) |

24,739 | Creditors and other payables | (15,455) |

(2,849) | Provisions | 5,398 |

3,155 | Employee entitlements | 3,543 |

(32,512) | Working capital movements – net | 37,521 |

Add/(less) items classified as investing or financing activities | ||

(4,940) | Biological assets revaluation loss/(gain) | 10,290 |

1,719 | Shares fair value decrease/(increase) | 1,084 |

– | Interest and dividends received | (344) |

3,185 | Net loss on sale or disposal of non current assets | 2,028 |

(36) | Total investing activity items | 13,058 |

120,105 | Net cash flow from operating activities | 189,122 |

Note 19: Adjustment arising on transition to the new PBE accounting standards

Reclassification adjustments

There has been no reclassification on the face of the financial statements in adopting the new PBE accounting standards.

Recognition and measurement adjustments

The department elected to early adopt PBE IPSAS 32 Service Concession Arrangement – Grantor in its 2013 financial statements. As a result no recognition and measurement adjustments were required to the financial statements for the year ended 30 June 2015 including comparatives.

The department reviewed all its revenue streams to determine whether the revenue is exchange or non-exchange. There were no recognition or measurement adjustments required as a result of this review.

Note 20: Related party disclosure

The department is a wholly owned entity of the New Zealand Crown. The Government significantly influences the strategic direction, operating intentions and business operations of the department as well as being its major source of revenue.

Related party disclosures have not been made for transactions with related parties that are within a normal supplier or client/recipient relationship on terms and conditions no more or less favourable than those that it is reasonable to expect the department would have adopted in dealing with the party at arms’ length in the same circumstances. Further, transactions with other government agencies (for example, government departments and Crown Entities) are not disclosed as related party transactions when they are consistent with the normal operating arrangements between government agencies and undertaken on the normal terms and conditions for such transactions.

The department has determined key management personnel as the Chief Executive and the individual members of the Executive Leadership Team. During the year legal services were purchased from Minter Ellison Rudd Watts. A partner of this legal firm is the brother of a member of the department’s Executive Leadership Team. The partner was not involved in providing any advice to the department. Purchases during the year totalled $0.025 million (2014: $0.003 million) and the transactions were conducted under normal arms’ length commercial terms. There is a nil balance outstanding at 30 June 2015 (2014: Nil).

The department has not entered into any commitments with any related parties.

The Treasury advises that responsible Minister Hon Peseta Sam Lotu-Iiga (effective 8 October 2014) and previously Minister Hon Anne Tolley have certified that they have no related party transactions for the year ended 30 June 2015 (2014: Minister Hon Anne Tolley – Nil).

Remuneration applicable to key management personnel is disclosed under Note 21.

Note 21: Key management personnel compensation

The department’s key management personnel are the six members of the Executive Leadership Team (2014: six), which include the Chief Executive, four Deputy Chief Executives and the National Commissioner.

2014 Actual $000 | 2015 Actual $000 | |

2,065 | Executive Leadership Team remuneration | 2,195 |

2,065 | Total key management personnel compensation | 2,195 |

Note 22: Post-balance date events

The department ‘Stepped-in’ to the management of the Mount Eden Corrections Facility (MECF) on 27 July 2015. MECF is operated under contract to the department by Serco. The decision to Step-in arises from incidents and events at MECF before and after balance date. The Step-in process may result in financial implications under the contract, including the recovery of Step-in costs. As of the date the financial statements were authorised for issue the financial and non-financial implications had yet to be determined, however, it is unlikely that these would have a material impact on the financial statements or performance information for the period ended 30 June 2015. Accordingly, no adjustment has been made, or is considered appropriate, to the 2014/15 financial statements or performance information as a result of the Step-in.

There were no other post-balance date events that required adjustment to the financial statements.

Note 23: Financial instruments

The department is party to financial instrument arrangements as part of its everyday operations. These include instruments such as cash and cash equivalents, investments, debtors and other receivables, creditors and other payables and other financial liabilities.

Fair value

The department uses various methods in estimating the fair value of a financial instrument. Fair values are determined according to the following hierarchy:

- quoted market price – financial instruments with quoted market prices for identical instruments in active markets

- valuation technique using market observable inputs – financial instruments with quoted prices for similar instruments in active markets or quoted prices for identical or similar instruments in inactive markets and financial instruments valued using models where all significant inputs are observable

- valuation technique with significant non-market observable inputs – financial instruments valued using models where one or more significant inputs are not observable.

The following table analyses the basis of the valuation of classes of financial instruments measured at fair value on the balance date:

Quoted market price $000 | Total $000 | |

As at 30 June 2015 | ||

Local currency financial assets | ||

Cash and cash equivalents (Note 6) | 58,459 | 58,459 |

Investments (Note 9) | 6,064 | 6,064 |

Total local currency financial assets | 64,523 | 64,523 |

As at 30 June 2014 | ||

Local currency financial assets | ||

Cash and cash equivalents (Note 6) | 82,337 | 82,337 |

Investments (Note 9) | 7,130 | 7,130 |

Total local currency financial assets | 89,467 | 89,467 |

Market risk

Price risk

Price risk is the risk that the fair value of future cashflows of a financial instrument will fluctuate as a result of changes in market prices. The department is exposed to price risk on its investments. The price risk is nominal as the investments are held by the department as a result of business dealings with the farming industry and, as such, are not expected to be traded and are not used to support cashflows.

Currency risk

Currency risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate due to changes in foreign exchange rates.

The department does not enter into forward foreign exchange contracts, as it engages in few overseas transactions, and is therefore only nominally susceptible to foreign exchange risks.

The department has no assets or liabilities that are denominated in foreign currency.

Interest rate risk

Fair value interest rate risk is the risk that the value of a financial instrument, or the cash flows from a financial instrument, will fluctuate, due to changes in market interest rates.

The department’s other financial liabilities primarily relate to its service concession arrangement which is interest bearing at the effective interest rate of 6.1% per annum. There is no interest rate risk exposure at balance date as the interest rate is fixed until August 2019.

The department has obtained ministerial approval for borrowing in relation to its service concession arrangement.

Credit risk

Credit risk is the risk that a third party will default on its obligations to the department, causing the department to incur a loss. In the normal course of business, the department is exposed to credit risk from trade debtors, transactions with financial institutions and the New Zealand Debt Management Office (NZDMO).

The department is only permitted to deposit funds with Westpac New Zealand Limited, or with the NZDMO, as these entities have high credit ratings. For other financial instruments, the department does not have significant concentrations of credit risk.

The department’s maximum credit risk exposure for each class of financial instrument is represented by the total carrying amount of cash and cash equivalents (Note 6) and debtors and other receivables (Note 7) presented in the Statement of Financial Position. There is no collateral held as security against these financial instruments, including those instruments that are overdue or impaired.

Credit quality of financial assets

The credit quality of financial assets that are neither past due nor impaired can be assessed by reference to Standard and Poor’s credit ratings (if available) or to historical information about counterparty default rates:

2014 Actual $000 | 2015 Actual $000 | |

Counterparties with credit ratings | ||

Cash and cash equivalents (Note 6) | ||

82,337 | AA- | 58,459 |

82,337 | Total cash and cash equivalents | 58,459 |

Investments (Note 9) | ||

7,130 | A+ | 6,064 |

7,130 | Total investments | 6,064 |

Counterparties without credit ratings | ||

Debtors and other receivables (Note 7) | ||

388,340 | Existing counterparty with no defaults in the past | 344,202 |

388,340 | Total debtors and other receivables | 344,202 |

Liquidity risk

Liquidity risk is the risk that the department will encounter difficulty raising liquid funds to meet commitments as they fall due.

In meeting its liquidity requirements, the department closely monitors its forecast cash requirements with expected cash draw downs from the NZDMO. The department maintains a target level of available cash to meet liquidity requirements.

Contractual maturity analysis of financial liabilities

The table below shows the department’s financial liabilities that will be settled based on the remaining period at the balance date to the contractual maturity date. The amounts disclosed are the contractual undiscounted cash flows.

Other financial liabilities mainly represent the department’s service concession arrangement with SecureFuture Wiri Limited. Repayment of the liability will be over a term of 25 years from service commencement at an effective interest rate of 6.1% per annum. The department has no securities against other financial liabilities. The value of the service concession arrangement asset is greater than the liability due to the asset including existing department owned land and other internally generated costs.

The department has entered into an agreement with Next Step Partners LP to design, rebuild, finance and maintain the maximum security Auckland East section of Auckland Prison under a Public Private Partnership (PPP). Other financial liabilities include $8.6 million of design and site development works completed to date under an Early Works Agreement, with a corresponding asset recognised under assets under construction.

The liability for the repayment of surplus to the Crown is not a financial liability as defined by PBE IPSAS 28 Financial Instruments: Presentation, as the obligation to pay arises from statute.

2014 Actual $000 | 2015 Actual $000 | |

Creditors and other payables (Note 13) | ||

119,749 | Less than six months | 104,294 |

Other financial liabilities | ||

300 | Less than one year | 10,562 |

25,800 | One to five years | 29,502 |

205,233 | More than five years | 280,196 |

351,082 | 424,554 | |

Categories of financial instruments

The carrying amounts of financial assets and financial liabilities in each of the PBE IPSAS 29 categories are as follows:

2014 Actual $000 | 2015 Actual $000 | |

Financial assets | ||

Loans and receivables | ||

82,337 | Cash and cash equivalents (Note 6) | 58,459 |

388,340 | Debtors and other receivables (Note 7) | 344,202 |

470,677 | Total cash and receivables | 402,661 |

Fair value through total comprehensive revenue and expense | ||

7,130 | Investments (Note 9) | 6,064 |

7,130 | Total investments | 6,064 |

477,807 | Total financial assets | 408,725 |

Financial liabilities | ||

Measured at amortised cost | ||

119,749 | Creditors and other payables (Note 13) | 104,294 |

231,333 | Other financial liabilities | 320,260 |

351,082 | Total financial liabilities | 424,554 |

Note 24: Capital management

The department’s capital is its taxpayers’ funds, which comprise general funds, revaluation reserves and fair value through other comprehensive revenue and expense reserves. Taxpayers’ funds are represented by net assets.

In accordance with the Public Finance Act 1989 (PFA) the department manages its revenue, expenses, assets, liabilities, investments and general financial dealings prudently and in a manner that promotes the current and future interests of the New Zealand public.

The department has asset management plans in place for major classes of assets detailing renewal and maintenance programmes.

The PFA requires the department to make adequate and effective provision in its long-term capital expenditure plans and that the department acts in accordance with financial delegations from Cabinet to the Chief Executive through the Responsible Minister. The PFA also requires that the department complies with the requirements of the State Sector Act 1988, Treasury Instructions and any other legislation governing its operations, when incurring any capital expenditure.

The objective of managing taxpayers’ funds is to ensure the department effectively achieves its goals and objectives for which it has been established, while remaining a going concern.

Note 25: Explanation of significant variances against Budget

Explanations for significant variances from the department’s budget are as follows:

Statement of Comprehensive Revenue and Expense

Crown revenue was higher than budget by $43.2 million mainly due to:

- the impact of asset revaluation of land and buildings as at 30 June 2014

- one-off funding received from the Justice Sector Fund to offset cost pressures mostly arising from the impact of the asset revaluation as at 30 June 2014 (depreciation) and costs associated with Auckland South Corrections Facility

- funding brought forward from 2015/16 in relation to Lifting Productivity and Performance in New Zealand’s Prisons.

Other revenue was higher than budget by $14.9 million mainly due to:

- higher offender employment activity revenue primarily driven by increased forestry logging volumes, favourable market prices for livestock sales and increased building refurbishment and catering activities, partly offset by lower milk prices

- insurance proceeds relating to the Christchurch earthquake and the Spring Hill Corrections Facility riot costs which were incurred in previous years

- profit on sale of assets.

Operating costs were higher than budget by $33.8 million mainly due to:

- contract management costs associated with service commencement at Auckland South Corrections Facility

- one-off project costs to transfer all Electronic Monitoring services to one supplier

- increased costs associated with offender employment activities, in particular higher logging volumes, and increased building refurbishment and catering activities

- loss on sale of assets

- remeasurement loss due to livestock quantity movement.

Depreciation and amortisation was lower than budget by $11.5 million due to the reprioritisation of capital projects and the deferral of capital expenditure to 2017/18.

Capital charge was higher than budget by $17.3 million mainly due to the revaluation of land and buildings as at 30 June 2014.

Statement of Financial Position

Cash and cash equivalents were significantly lower than budget to align with Treasury’s best practice of minimising cash surpluses.

Debtors and other receivables were higher than budget by $161.5 million mainly due to an increase in debtor Crown, as a consequence of the department requiring less cash.

Property, plant and equipment was higher than budget by $121.5 million due to the revaluation gains on land and buildings as at 30 June 2014. The gains on buildings were mainly due to increases in construction costs and re-assessment of useful lives. This was partly offset by capital expenditure being deferred to 2017/18 and the sale of the Tongariro/Rangipo forest land on 30 June 2015.

Biological assets were lower than budget by $38.5 million mainly due to the sale of the Tongariro/Rangipo forest crop on 30 June 2015.

Creditors and other payables were higher than budget by $16.3 million due to the timing of accruals.

Total employee entitlements were higher than budget by $13 million mainly due to changes in actuarial valuations and higher rates of remuneration.

Total other financial liabilities were higher than budget by $10.6 million mainly due to the commencement of design and site development works at the maximum security Auckland East section of Auckland Prison.

General funds were lower than budget by $63.3 million mainly due to capital withdrawals during the year, in particular, proceeds from the Tongariro/Rangipo forest crop and land sale on 30 June 2015.

Reserves were higher than budget by $216 million mainly due to the revaluation gains on land and buildings as at 30 June 2014.